Original author: Dappradar

Original translation: Felix, PANews

Summer is over, and September is often a time of fresh starts, not only in daily life but also in the market. This year, a bull market arrived in the middle of summer, and the industry has clearly entered a new phase of growth.

On-chain activity may have cooled slightly in August, but the story beneath the surface is quite different. DeFi TVL hit a new all-time high, institutions entered the market en masse, NFTs heated up again, and AI dapps developed rapidly, even as the hype cycle shifted. At the same time, security incidents reminded us that the industry is still a work in progress.

The data clearly shows one thing: Web3 isn't standing still. As we head into autumn, the bull run is gaining momentum. This isn't just reflected in speculation, but also in adoption, innovation, and actual capital flowing into the chain.

Key Takeaways

- The number of daily active unique wallets (dUAW) fell 18% in August to 17 million, indicating that on-chain activity cooled off during the summer.

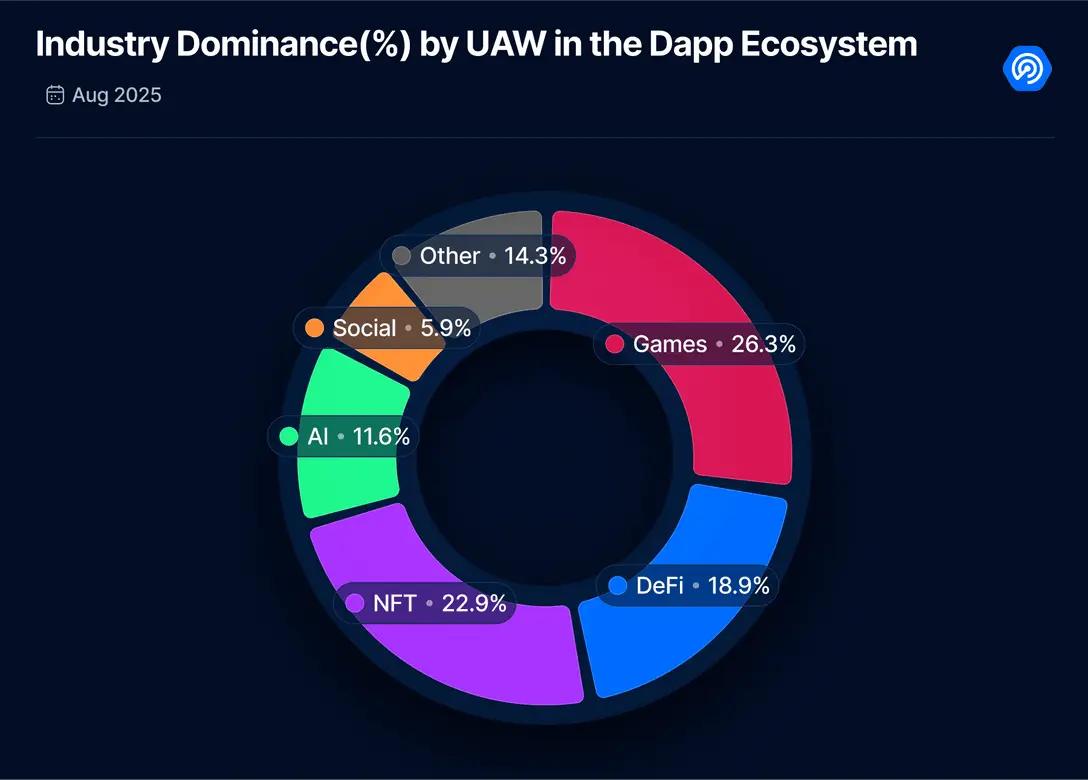

- Although gaming DApp activity dipped slightly by 4%, it still dominated, while NFTs rose by 7% and social DApps fell by 63%.

- Driven by Ethereum’s strong performance, DeFi TVL hit an all-time high of $292 billion in August, up 13% from July.

- The market capitalization of cryptocurrencies has hit new highs: the total market capitalization reached US$3.82 trillion, and non-BTC assets reached US$1.59 trillion, exceeding the 2021 peak.

- Ethena’s USDe supply grew 42% to $12.4 billion, generating $61 million in revenue, solidifying its position as DeFi’s most profitable stablecoin.

- NFT transaction volume increased by 9%, with Courtyard surpassing Ethereum blue-chip projects to lead all series.

- In August, losses due to vulnerabilities amounted to $159 million, a 20% increase from July. One phishing attack alone resulted in losses of $91 million.

Dapp cooling in August

On-chain activity cooled significantly in August. The number of daily active unique wallets (dUAW) in the Dapp industry fell 18% to 17 million.

Two categories were hit hardest: Social apps saw a 63% decline, and AI apps saw a 49% drop. While these declines are surprising, they are also natural cycles. Both categories experienced months of rapid growth and hype, but maintaining this momentum and engagement is a significant challenge. The promise of these two product categories remains exciting. In the long run, they could reshape the industry, but for now, these declines suggest that their development is still in its early stages.

On the other hand, other categories saw growth. NFT activity increased by 7%, reclaiming the dominant second place in the industry. This was a surprising rebound considering the market slowdown earlier this year. Despite a slight decrease in activity (4%), Gaming dapps regained their position as the most active sector, demonstrating the category's resilience as a pillar of on-chain engagement.

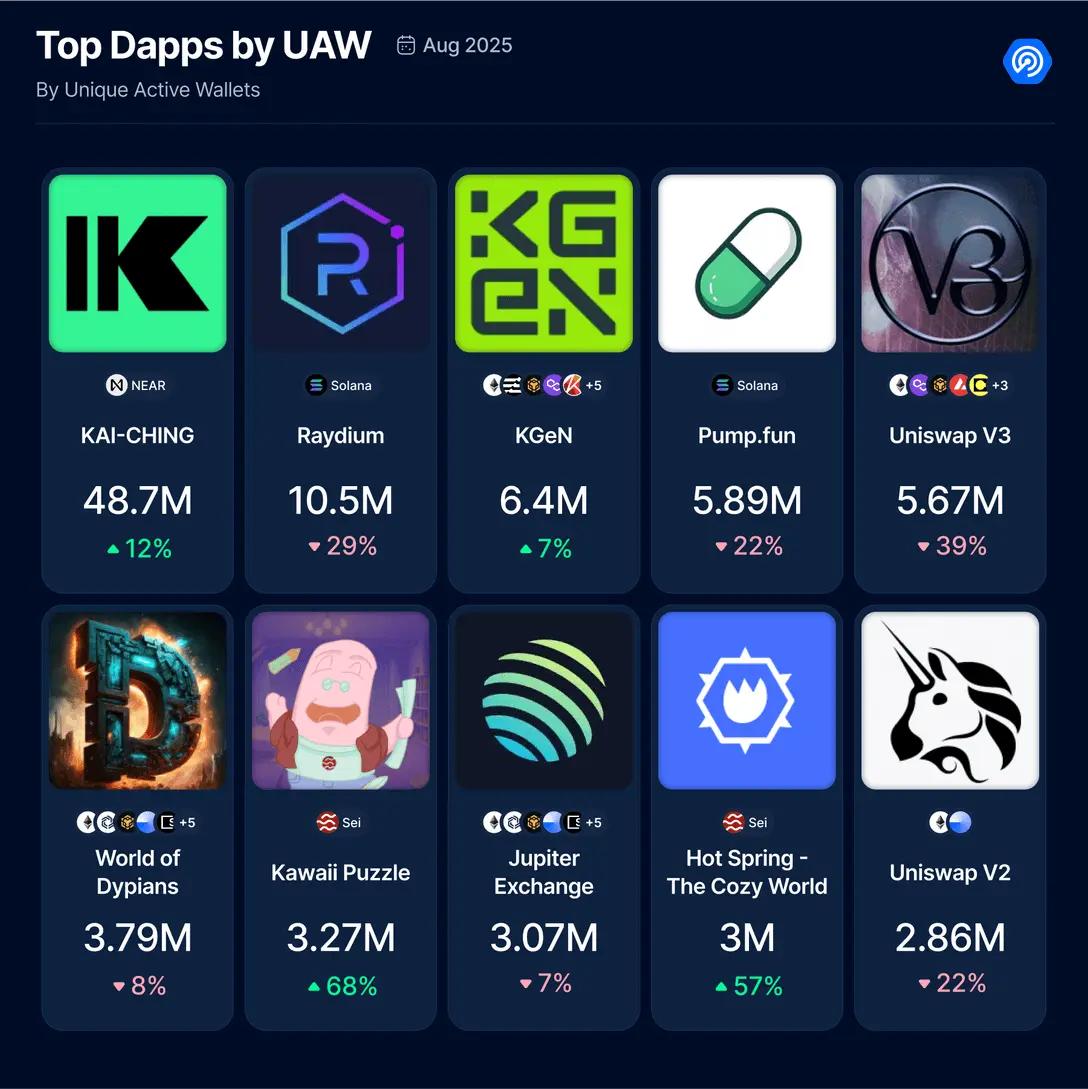

Looking at the most active Dapps in August, they span DeFi, gaming, social networking, and AI, but no single category has completely dominated. This highlights the current state of the industry: a diverse yet balanced ecosystem where each sector is exploring its unique strengths.

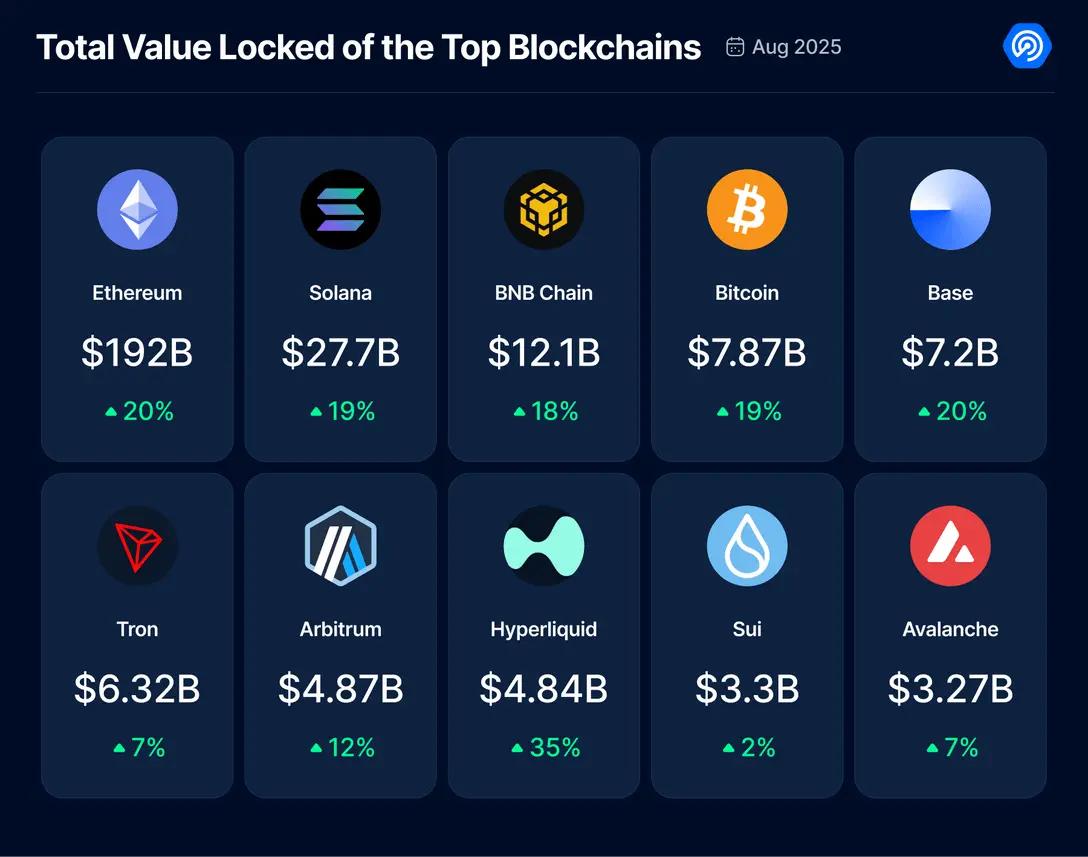

DeFi TVL hits new high, with institutions entering the market

In August, DeFi's performance confirmed what many had previously speculated. DeFi's TVL reached $292 billion, a 13% increase from July, primarily driven by Ethereum's strong performance. Both DeFi TVL and ETH prices hit all-time highs in August, highlighting the industry's strong momentum.

Looking at the entire crypto market, the overall market also shows strong momentum:

- The total market capitalization of cryptocurrencies, including BTC, rose 4% in 30 days to $3.82 trillion, a record high.

- The total market capitalization of cryptocurrencies excluding BTC rose 15% to $1.59 trillion, just above the peak reached in November 2021.

- The total market capitalization of cryptocurrencies excluding BTC and ETH rose 9.41% to $1.05 trillion, also a new high.

The takeaway? Ethereum continues its hypergrowth, while Altcoin remain largely subdued. However, with Altcoin market capitalization up just 12% since the beginning of the year, we may be in the middle of a bull run, the period before Altcoin typically begin to accelerate upwards.

In addition to market data, August also saw a series of product and institutional milestones:

- Protocol Innovation: Uniswap's Unichain has enabled Flashblocks, achieving 200-millisecond block confirmations, comparable to CEX speeds and MEV-resistant. Base and other OP Stack chains have also adopted this upgrade through Flashbots. Furthermore, Pendle Finance launched Boros on Arbitrum, allowing users to trade perpetual funding rates directly on-chain. Finally, Synthetix announced its return to the Ethereum mainnet and the launch of a new perpetual contract exchange, demonstrating that the L1-L2 hybrid experiment is far from over.

- Institutional Adoption: Aave Labs launched Horizon, an institutional lending platform that provides access to tokenized Treasuries and RWAs. Aave Horizon has already attracted institutional investors such as VanEck, WisdomTree, Hamilton Lane, Circle, and Ethena. Furthermore, Ripple's RLUSD stablecoin has joined Horizon's risk asset market, expanding collateral options. Meanwhile, Chainlink further solidified its position as the core data layer for crypto by integrating FX and precious metals data from the Intercontinental Exchange (ICE), connecting TradFi-grade data to DeFi infrastructure.

- Stablecoins and Yields: Ethena’s USDe supply surged 42% to $12.4 billion, with protocol revenue reaching a new high of $61 million in August. Its rapid growth has solidified USDe as one of the most profitable and controversial stablecoin models in DeFi, and has sparked ongoing discussions about sustainability and fee capture.

This bull run feels different. Unlike past cycles, institutions are now shaping the market narrative and infrastructure. Market growth is no longer driven by retail investors, but by innovative financial products, investment funds, and governments embracing the technology.

AI DApps’ popularity cooled in August

AI has become one of the most transformative forces today, reshaping not only technology but also everyday life. However, within the blockchain sector, August saw a slowdown. As mentioned in the industry overview, AI DApp activity dropped 49%, demonstrating that even the hottest sectors are not immune to cyclical fluctuations. However, top AI projects continue to rank highly, and new entrants continue to push the boundaries of what's possible.

New AI protocols added this month include:

Vibely: An AI companion designed to alleviate loneliness and anxiety.

Calories Cash: A Telegram-based AI agent that allows users to take photos of the food they eat to get calorie estimates and earn token rewards.

But the headlines this month came from Numerai, a decentralized hedge fund built entirely on machine learning models contributed by thousands of data scientists. Numerai secured $500 million in funding from JPMorgan Asset Management, nearly doubling its assets under management and sending its NMR token soaring over 100% in a matter of days. The fund's performance is driven by AI models staked with NMR, meaning JPMorgan's backing represents not only an influx of capital but also a validation of AI-driven asset management coordinated through blockchain incentives.

On the infrastructure level, the Render Network is entering the AI space by piloting US-based computing services and introducing high-end GPUs to support decentralized machine learning. This expansion beyond graphics rendering makes Render a strong competitor to cloud giants, and node operators will receive RNDR rewards. Similarly, Bittensor has launched a new governance module (dTAO), giving token holders more control over upgrades and strengthening the TAO's coordinating role in the decentralized AI ecosystem.

The Artificial Super Intelligence (ASI) Alliance, comprised of Fetch.ai, SingularityNET, and Ocean Protocol, is focused on developer engagement. An August hackathon showcased AI agent use cases ranging from DeFi automation to decentralized data sharing. While the FET token remains stable, the ecosystem's $50 million buyback program and collaborative governance framework provide a solid foundation for long-term growth.

Bottom line: Even as adoption has cooled, AI in crypto continues to grow rapidly. Institutional capital, decentralized infrastructure, and an active community are now driving the field’s evolution, demonstrating that this isn’t just hype, but rather the ongoing construction phase of decentralized AI.

NFT momentum is strong, Courtyard makes history

The NFT market continued to gain momentum in August. Trading volume increased by 9%, despite a 4% decrease in the number of NFT sales, indicating that while fewer assets were trading, collectors were paying higher prices for each transaction.

This makes July and August the two strongest months for NFT trading volume and sales since February 2025. All signs point to a return to the NFT space. This resurgence stems in part from mainstream adoption. In Ibiza, the world-renowned nightclub Hi, in partnership with The Night League and London's W1 Curates, opened the first permanent NFT art gallery within the club. The immersive digital installation showcases works by renowned crypto artists such as Beeple, Mad Dog Jones, WhIsBe, and KidEight, signaling that NFTs are breaking out of the Web3 sphere.

Another driver is Base, whose low minting costs and speculation around an upcoming airdrop have boosted NFT activity. Base has now climbed to the third most traded chain, highlighting how scaling solutions can impact NFT adoption.

Ethereum remains strong, dominating the NFT industry with a 61% market share. In August, developers introduced ERC-8004, a proposed standard for using NFTs as unique on-chain identifiers for autonomous programs. This will enable AI systems and decentralized applications to securely identify and interact with each other using an NFT-based ID and reputation layer.

Elsewhere, Solana made progress in scalability, successfully conducting a stress test exceeding 100,000 transactions per second, 10 times the previous average. This move positions Solana as a strong contender for hosting large-scale NFT and gaming markets. On the product front, Solana's wallet, Phantom, acquired the NFT analytics platform Solsniper, with plans to integrate its wallet tracking and scrambling tools into the Phantom app.

On the market side, Blur surpassed OpenSea, capturing 22% of total NFT trading volume, thanks to its active rollout of new features and liquidity incentives. Meanwhile, OpenSea launched a beta version of its Model Context Protocol (MCP) server, an open standard that provides real-time NFT and wallet data to AI applications on over 20 chains, placing it at the intersection of NFTs and AI.

On the collectibles front, the biggest surprise came from Courtyard, which became the most traded NFT collectible, surpassing even Ethereum's blue-chip projects. Courtyard's momentum was bolstered by a $30 million Series A funding round in late July, which aims to expand its model of bringing real-world collectibles on-chain, providing instant liquidity and verifiable provenance. Courtyard's rise, along with platforms like Phygitals on Solana, suggests that RWAs will become the dominant NFT trend in the second half of 2025.

Blue-chip collaborations also made headlines. Azuki partnered with Swiss watchmaker H. Moser & Cie. to launch "Elements of Time," a series of luxury watches connected to Ethereum. Each watch comes with an NFT-based Physical Backing Token (PBT) to verify its authenticity and ownership.

Generative art also reached a milestone. Art Blocks announced the upcoming launch of its 500th project and celebrated its fifth anniversary. The "Art Blocks 500" series, slated for November, will cover all six categories and mark the end of its Curated series, heralding the end of the first era of on-chain generative art.

The conclusion? The NFT market is heating up again.

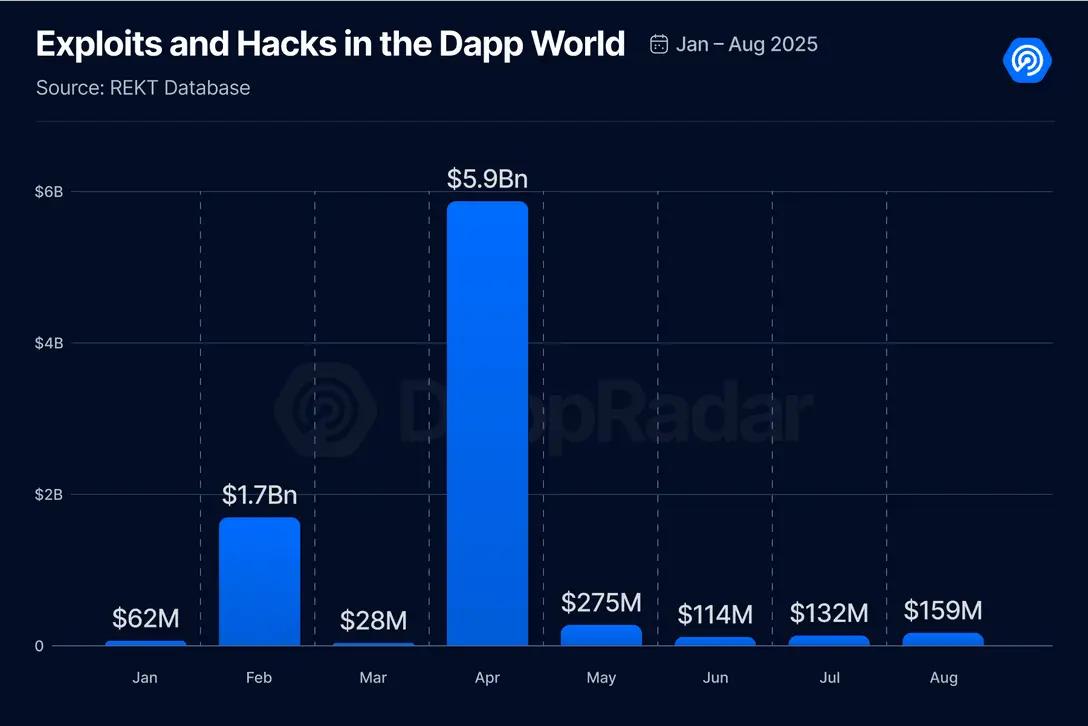

Web3 attacks increased by 20% in August

August was another difficult month for Web3 security. According to the REKT database, losses from hacker attacks and exploits reached $159 million, a 20% increase from July. However, compared to previous months, August's figures were modest.

The most notable incident in August was a massive phishing attack, accounting for 57% of total losses. Victims lost 783 Bitcoin (approximately $91 million) in a sophisticated social engineering scam in which attackers impersonated customer service representatives from exchanges and hardware wallets. This theft occurred a year after the Genesis creditor exploit resulted in $243 million in losses. The stolen funds were laundered through privacy-focused mixers such as Wasabi Wallet.

The second-largest incident occurred at the Turkish exchange BtcTurk, which suffered a suspected hacker attack, resulting in losses estimated at $48 to $50 million. The stolen funds originated from the platform's hot wallet. While deposits and withdrawals were suspended during the investigation, local fiat currency transactions and trading services remained normal.

Another high-profile attack targeted Odin.fun, a Bitcoin-based memecoin issuance and trading platform, where attackers manipulated liquidity in its automated market-making tool and stole 58.2 Bitcoin (approximately $7 million).

This month has once again highlighted the importance of security awareness in Web3. From phishing to hot wallet thefts, attackers are constantly evolving their tactics. Be sure to protect your assets, carefully verify the source of your communications, and use secure storage methods.

Conclusion

August highlighted the continued vitality of the DApp industry. While overall activity cooled, DeFi TVL soared to a new all-time high, NFTs regained momentum, and AI dapps continued to attract institutional attention despite declining usage. At the same time, security incidents highlight the importance of vigilance now more than ever.

However, it's important to note that this cycle is "different." Institutions are no longer sitting on the sidelines, but are actively shaping the market through capital, partnerships, and infrastructure. As we enter the final quarter of 2025, the interplay between retail trends, institutional adoption, and technological breakthroughs will determine the future direction of the industry.

One thing is clear: on-chain innovation is not slowing down.

Click here to learn about ChainCatcher's current job openings

Recommended reading:

After its stock price halved, will Metaplanet continue its Bitcoin bet?

Understanding WLFI in One Article: Using USD1 to Connect Stablecoins and Traditional Capital Markets

Question 5: What is good DeFi? ARK’s answer and the path to on-chain autonomy