Founding Partner, SOFA.org

Augustine Fan is a professional with over two decades of distinguished experience, active in Wall Street, family offices, private equity, and now in the cryptocurrency space. He currently holds leadership positions at SOFA.org and is also a partner and CFO at SignalPlus, a leading digital asset software technology provider in the cryptocurrency options space.

Prior to entering the cryptocurrency space, Augustine worked at Goldman Sachs for ten years as a US interest rate trader and macro expert, serving in New York, London, Tokyo and Hong Kong offices. After leaving Wall Street, he joined a shipping-based family office in Hong Kong, helping to manage one of the most active sub-macro trading portfolios in Asia. He then became the Chief Investment Officer (CIO) of another family office in Hong Kong, focusing on private equity, credit, real estate, listed companies and frontier market investments.

Augustine is a CFA, Leslie Wong Fellow, and graduated with First Class Honours from the University of British Columbia (UBC) in Canada with a Bachelor of Commerce degree.

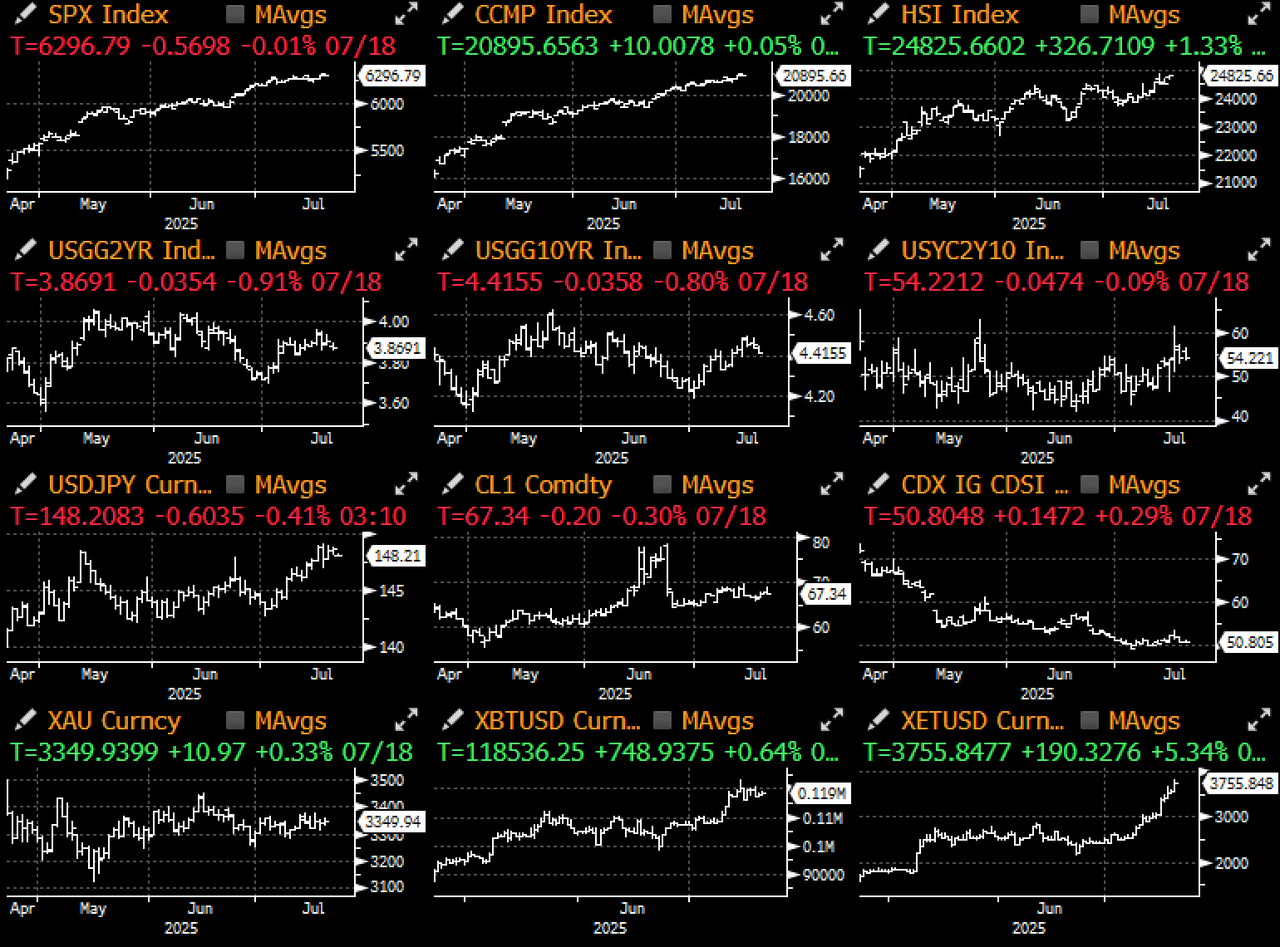

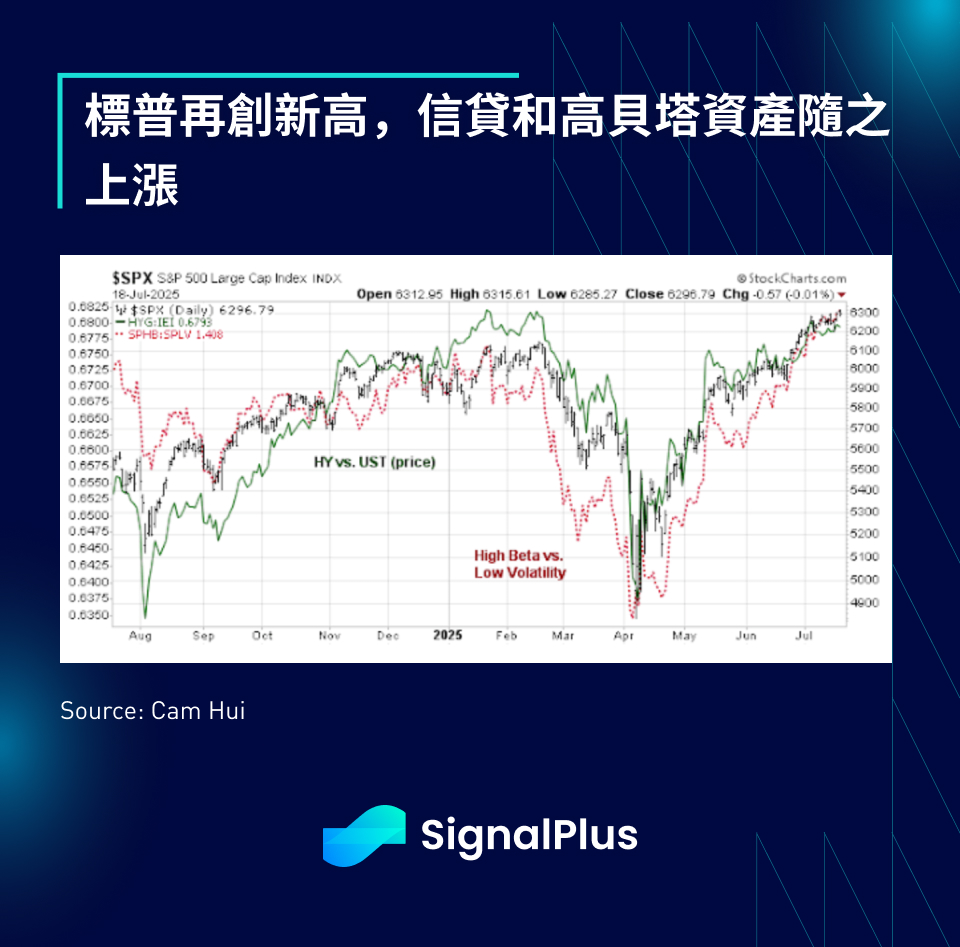

Another week, another all-time high. The S&P 500 hit another all-time high on Friday, the third time this week and the sixth time in July. The market continues to ignore the ongoing tariff escalation (30% tariffs on Mexico and the EU), the initial transmission of price pressures in the latest CPI data, and the latest farce of removing Fed Chairman Powell for "just cause".

The recent rally has pushed the S&P 500's price-to-earnings ratio close to its own all-time high, just as the second-quarter earnings season is about to kick off and investors are paying a premium for any kind of stock exposure.

Meanwhile, encouraged by the stock market's performance, President Trump has reignited his tariff escalation war and is making plans to add industry-specific tariffs on top of existing country-specific tariffs, which will reportedly be implemented within two weeks. The initial target industries will be pharmaceuticals and semiconductors, aiming to fully cover US imports.

Despite the new threats, markets have almost completely ignored this round of tariff escalation, with “tariff-sensitive” thematic sectors continuing to underperform the benchmark index. Whether due to expectations of an eventual “TACO” moment (referring to the easing of trade tensions), less targeted attacks on key trading partners (the expected Trump-Xi summit in South Korea), or confidence that the private sector can handle the shock, markets are likely to remain deaf to the trade conflict until further notice.

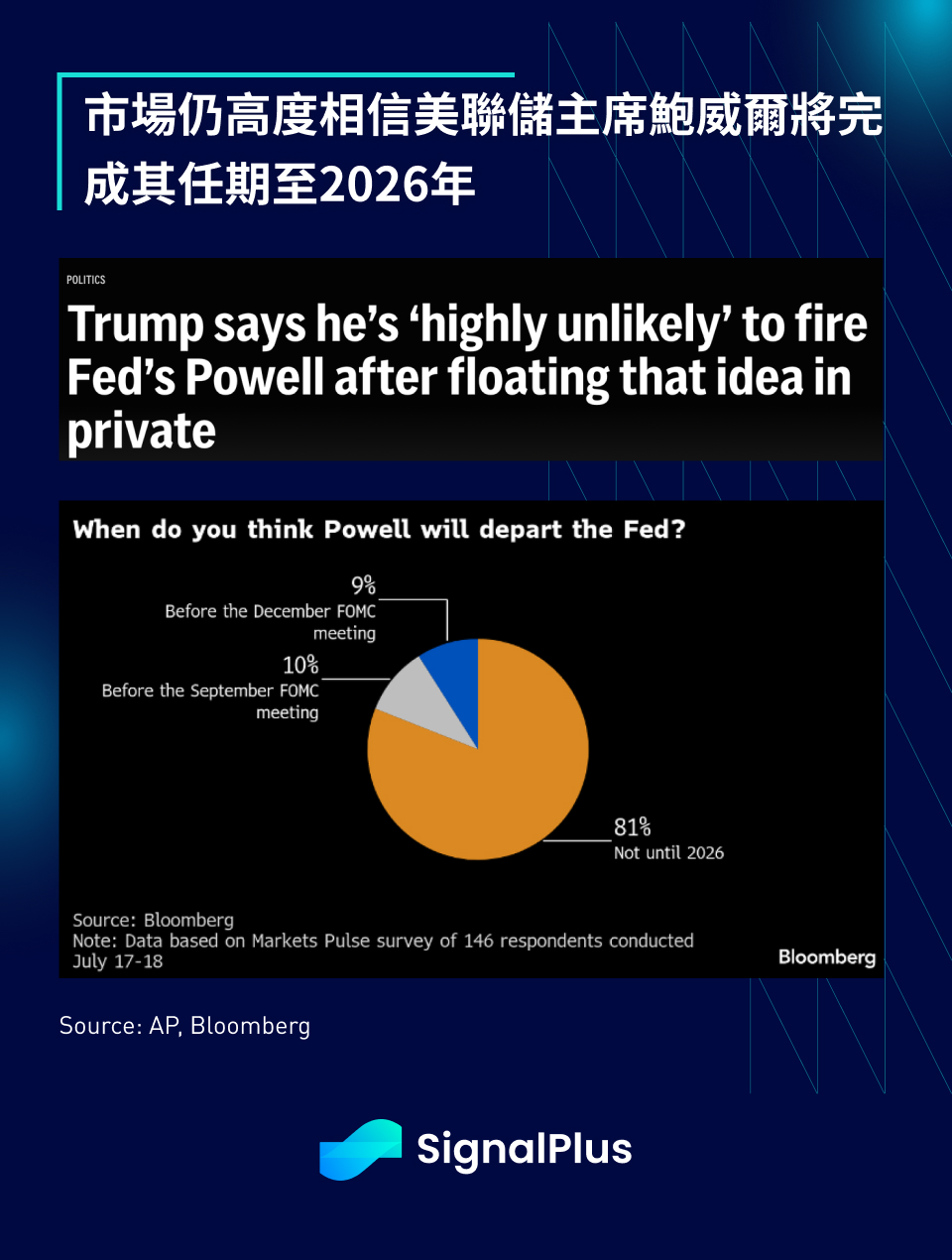

Speaking of policies, the Trump administration has set off a new round of Fed turmoil, with media reports saying that Fed Chairman Powell may be removed due to serious budget overruns for building renovations. Yes, you read that right!

Powell has been entangled in project management issues over some of the roughly $2.5 billion renovations to the Fed’s Washington headquarters that have cost about $600 million more than initially expected. Asked Tuesday whether the costly renovations constituted a fireable offense, Trump said, “I think to some extent, yes.” — The Hill

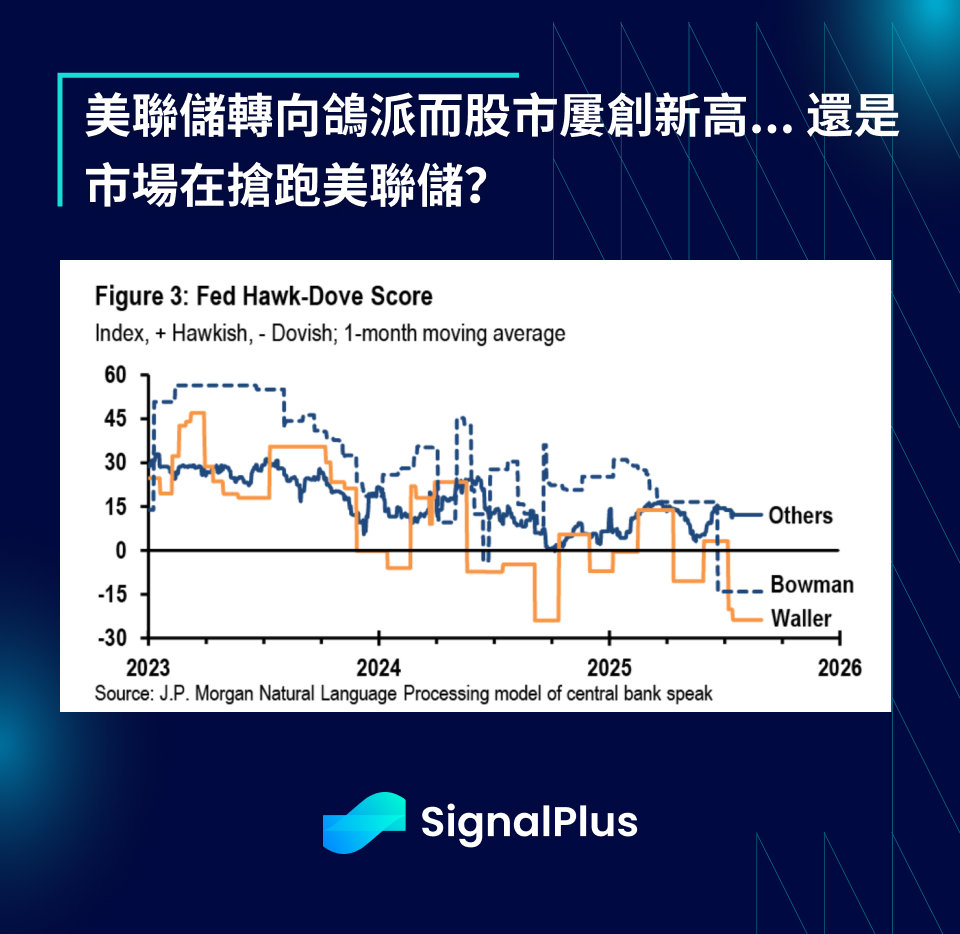

Is it any wonder that the market is in the same risk-on mode it has been in for the past two months as the Fed rhetoric turns dovish and stocks continue to hit new highs? Or is the market pricing in a dovish Fed, front-running the upcoming rate cuts and contributing to the Goldilocks economics narrative?

Data from the past week also aligned well, with the University of Michigan reporting a slight improvement in consumer confidence both about current conditions and future expectations, while one-year inflation expectations have fallen to pre-tariff levels (4.4% vs. 5.0% prior).

Surprisingly, despite the market’s continued rally, we haven’t seen extreme sentiment readings in traditional momentum indicators: the National Association of Individual Investors bull-bear ratio remains around the mid-range, and search engine queries for “boom” stories remain at historically low levels.

Are the macro doomsayers finally extinct? Have we all accepted the belief that the stock market can only go up and not down? Don’t short the short the trend…

The crypto space certainly hasn’t missed out on our own FOMO moment. Ethereum is having a blast, approaching the $4,000 region (up 22% in 5 sessions), with some major Altcoin also posting double-digit gains this week. Bitcoin has also hit its own all-time high, topping $118,000, though the excitement has been a little restrained. Until further notice, it feels like the good times are back.

The ETH/BTC ratio has temporarily risen from the grave and has improved to its best level since Q1. Some attribute this to the focus on stablecoins/real world assets being good for proof-of-stake networks, while others see Ethereum's new treasury strategy as a catalyst for the rise. We personally believe this is just a classic risk-on spillover, as most of the money in mainstream traditional finance has been fully deployed in Bitcoin over the past 7 months.

At the risk of repeating what I have said for most of the past 8 weeks… Never short a dull market, and enjoy the good times rolling in. Good luck and happy trading to all of you as we head into the hot summer months!

Risk Warning

Cryptocurrency investment carries a high degree of risk. Its price may fluctuate drastically and you may lose all your capital. Please assess the risk carefully.