Original Title: The Hidden Mechanics Behind Ethereum's Rally: Understanding Market Structure and Systemic Risk

Source: A1 Research

Translated by: Tim, PANews

Ethereum's price fluctuations seem simple: retail enthusiasm is high, prices surge, and market optimism continues to ferment. However, beneath the surface, there are complex market mechanisms. The interplay between funding rate markets, hedging operations of neutral strategy institutions, and recursive leverage demands expose deep systemic vulnerabilities in the current crypto market.

We are witnessing a rare phenomenon: leverage has essentially become liquidity itself. The massive long positions invested by retail investors are fundamentally reshaping how neutral capital allocates risk, thereby giving birth to new market vulnerabilities that most market participants have not yet fully recognized.

1. Retail Follow-up Long Phenomenon: When Market Behavior is Highly Homogeneous

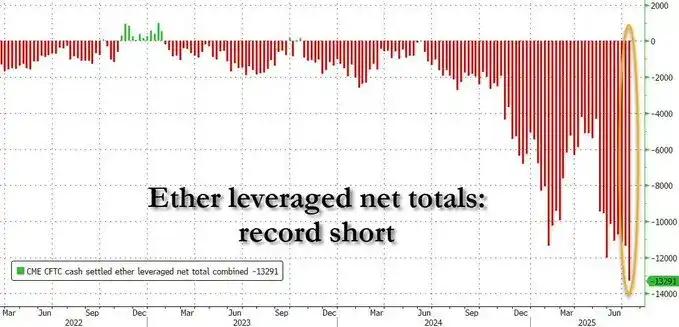

Retail demand is concentrated in Ethereum perpetual contracts because these leveraged products are easy to access. Traders are rushing into long leveraged positions at a speed far exceeding spot real demand. The number of people wanting to bet on ETH's rise far exceeds those actually purchasing Ethereum spot.

These positions require counterparties. However, due to abnormally aggressive buying demand, short positions are increasingly being absorbed by institutional players executing Delta neutral strategies. These are not directional bearish players, but rather funding rate harvesters who intervene not to short ETH, but to arbitrage structural imbalances.

In fact, this is not shorting in the traditional sense. These traders hold an equal amount of spot or futures long positions while shorting perpetual contracts. As a result, they do not bear ETH price risk but earn income from the funding rate premium paid by retail longs to maintain leveraged positions.

As Ethereum ETF architecture evolves, this arbitrage trading may soon be enhanced by overlaying passive income layers (staking yield embedded in ETF packaging), further strengthening the attractiveness of Delta neutral strategies.

This is indeed a brilliant trade, provided you can tolerate its complexity.

Delta Neutral Hedging Strategy: Response Mechanism of Legitimate "Money Printing"

Traders take on retail long demand by shorting ETH perpetual contracts while hedging with spot long positions, thus converting the structural imbalance caused by continuous funding rate demand into profit.

In a bull market, funding rates turn positive, with longs paying fees to shorts. Institutions adopting neutral strategies earn income by providing liquidity while hedging risks, forming a profitable arbitrage operation that attracts continuous institutional capital.

However, this creates a dangerous illusion: the market seems deep and stable, but this "liquidity" depends on favorable funding environments.

The moment the incentive mechanism disappears, its supporting structure will collapse. Surface market depth will instantly turn to void, and prices may violently fluctuate as the market framework collapses.

This dynamic is not limited to crypto native platforms. Even on the Chicago Mercantile Exchange dominated by institutions, most short liquidity is not directional betting. Professional traders short CME futures because their investment strategies prohibit spot exposure.

Options market makers hedge Delta through futures to improve margin efficiency. Institutions hedge institutional customer order flows. These are structural necessary trades, not bearish expectations manifestations. Uncleared contract volume may rise, but this rarely conveys market consensus.

Asymmetric Risk Structure: Why It's Actually Unfair

Retail longs directly face liquidation risk when prices move unfavorably, whereas Delta neutral shorts are usually better-funded and managed by professional teams.

They pledge held ETH as collateral and can short perpetual contracts in a fully hedged, capital-efficient mechanism. This structure can safely bear moderate leverage without triggering liquidation.

There are structural differences. Institutional shorts have persistent resilience and comprehensive risk management to withstand volatility; leveraged retail longs have weak capacity and scarce risk control tools, with almost zero operational error tolerance.

When market conditions change, longs will quickly disintegrate while shorts remain solid. This imbalance can trigger a liquidation cascade that seems sudden but is structurally inevitable.

Recursive Feedback Loop: When Market Behavior Becomes Self-Interfering

Continuous long demand in Ethereum perpetual contracts requires Delta neutral strategy traders to act as counterparties for short hedging, maintaining funding rate premium. Various protocols and yield products compete to chase these premiums, driving more capital back into this circular system.

A perpetually money-making machine does not exist in reality.

This will continue to create upward pressure, but entirely depends on one premise: longs must be willing to bear leverage costs.

The funding rate mechanism has an upper limit. On most exchanges (like Binance), perpetual contract funding rates are capped at 0.01% every 8 hours, equivalent to an annualized yield of about 10.5%. When this limit is reached, even if long demand continues, shorts seeking returns will no longer be incentivized to open positions.

Risk accumulation reaches a critical point: arbitrage returns are fixed, but structural risks continue growing. When this critical point arrives, the market will likely liquidate rapidly.

Why ETH Crashes Harder Than BTC: Dual Ecosystem Narrative Conflict

Bitcoin benefits from non-leveraged buying from corporate fiscal strategies, and BTC derivatives market already has stronger liquidity. Ethereum perpetual contracts are deeply integrated into yield strategies and DeFi protocol ecosystems, with ETH collateral continuously flowing into structured products like Ethena and Pendle, providing yield returns for users participating in funding rate arbitrage.

Bitcoin is typically considered driven by natural spot demand from ETFs and corporations. However, a large part of ETF capital flow is actually a mechanical hedging result: traditional financial basis traders buy ETF shares while shorting CME futures contracts to lock in and arbitrage the fixed spread between spot and futures.

This is essentially identical to ETH's Delta neutral basis trading, just executed through regulated packaging structures and financed at 4-5% USD cost. From this perspective, ETH leverage becomes a yield infrastructure, while BTC leverage forms structured arbitrage. Neither are directional operations; both aim to generate returns.

Circular Dependency Issue: When the Music Stops

Here's a question that might keep you up at night: This dynamic mechanism has an inherent cyclical nature. Delta neutral strategy profitability depends on continuous positive funding rates, requiring sustained retail demand and bull market environment.

Funding rate premiums are not permanent and are very fragile. When premiums contract, liquidation waves begin. If retail enthusiasm wanes and funding rates turn negative, shorts will pay longs instead of collecting premiums.

When large capital inflows occur, this dynamic mechanism creates multiple fragile points. First, as more capital enters delta neutral strategies, basis will continuously compress. As financing rates drop, arbitrage trading returns will correspondingly decrease.

If demand reverses or liquidity dries up, perpetual contracts might enter a discount state, with contract prices lower than spot prices. This would obstruct new Delta neutral positions and potentially force existing institutions to exit. Meanwhile, leveraged longs lack margin buffer space, and even mild market pullbacks could trigger cascading liquidations.

When neutral traders withdraw liquidity and long positions are forcibly liquidated like a waterfall, a liquidity vacuum is formed, with no true directional buyers below the price, leaving only structural sellers. The originally stable arbitrage ecosystem quickly flips, evolving into a chaotic liquidation wave.

Misreading Market Signals: The Illusion of Balance

Market participants often misinterpret hedging fund flows as a bearish tendency. In fact, ETH's high short positions often reflect profitable basis trading, rather than directional expectations.

In many cases, the seemingly strong derivatives market depth is actually supported by temporary liquidity leased by neutral trading desks, which earn revenue by harvesting funding premiums.

While spot ETF fund inflows can generate a certain degree of natural demand, most trades in the perpetual contract market are essentially structural human manipulations.

Ethereum's liquidity is not rooted in belief in its future, but exists as long as the funding environment is profitable. Once profitability dissipates, liquidity will also drain away.

Conclusion

The market can remain active for a long time under structural liquidity support, creating a false sense of security. But when conditions reverse and longs cannot maintain financing obligations, the collapse happens in an instant. One side is completely crushed, while the other withdraws calmly.

For market participants, identifying these patterns means both opportunity and risk. Institutions can profit by understanding funding conditions, while retail investors should distinguish between artificial and genuine market depth.

The driving factors of Ethereum's derivatives market are not consensus on decentralized computing, but structural behavior of harvesting funding rate premiums. As long as funding rates remain positive, the entire system can run smoothly. However, when the situation reverses, people will ultimately discover that the seemingly balanced appearance is nothing more than a carefully disguised leverage game.

Recommended reading:

US House Passes Three Crypto Bills, How is the National Team's BTC Chip Battle Going?

BitMine Stock Soars: Silicon Valley Venture Capital Godfather Peter Thiel Bets Big on Ethereum

From PayPal Mafia to Investment Empire: Unveiling the Rise of Peter Thiel's Founders Fund (Part One)